Executive Summary

- Harness Asia’s diverse markets and transformative growth drivers to navigate geopolitical uncertainties and shifting global policies.

- Strengthen your portfolio’s resilience and income potential by incorporating Asian dividend equities, defensive low-volatility strategies, and Asian bonds - all offering compelling yields, stable returns, and effective diversification in today’s volatile market environment.

- Unlock long-term growth opportunities by adopting a diversified Asian investment strategy, or by targeting high-potential single-country approaches that capitalise on unique macroeconomic trends and earnings cycles across the region.

When geopolitical developments, policy divergence as well as shifting growth and inflation dynamics intersect, the dispersion of returns across markets and styles widen. Against this backdrop, Asia’s powerful structural themes such as AI and technology, rising domestic consumption and corporate reforms create a rich and differentiated opportunity set. Meanwhile, the region’s diversity provides investors with multiple paths to targeted outcomes.

Income & capital growth

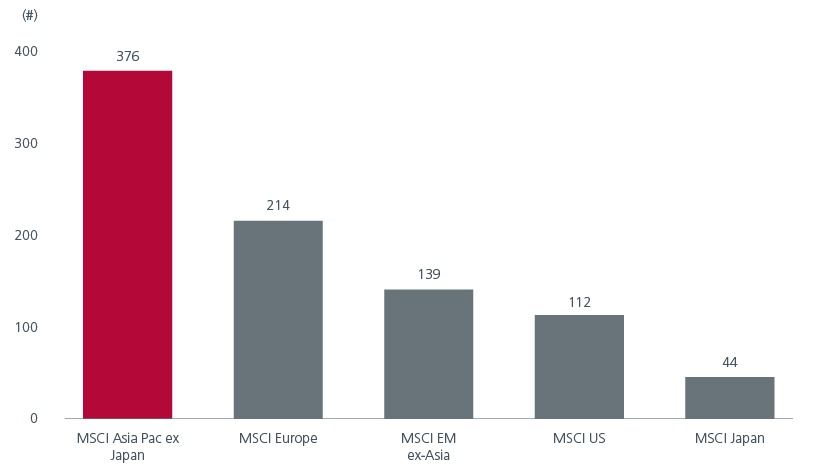

Asian equity income: Asian dividend equities offer one of the most compelling income opportunities globally. Compared to the rest of the world, Asia Pacific ex Japan has the highest number of companies (376) with dividend yields above 3%, reflecting a strong focus on shareholder returns. See Fig. 1. A higher composition of technology stocks in Asia’s high dividend yielding index suggests that an Asian equity income strategy can deliver both income and growth. An active approach can identify emerging income opportunities that may be missed by passive or screen‑based strategies, deliver incremental income through innovative strategies and identify risks to dividend sustainability.

Fig. 1. Asia has more companies with dividend yields above 3%

Source: Eastspring Investments, MSCI, as at 31 December 2025. The use of indices as proxies for the past performance of any asset class/sector is limited and should not be construed as being indicative of the future.

Low volatility equities: A low volatility strategy offers investors a more defensive way to access Asian equities. By systematically focusing on stocks with more stable price behaviour, low volatility strategies aim to reduce drawdowns and smooth returns over time - an attribute that is particularly valuable during periods of heightened uncertainty. In addition, by tilting towards more stable, cash‑generative companies, low volatility strategies can also deliver income, potentially providing attractive total returns for investors.

Singapore: The Singapore equity market offers a mix of blue-chip large caps – companies with stable business models which are relatively defensive, and a growing small and mid-cap universe that offers exposure to emerging growth sectors. As such, a strategy that allocates to both segments can potentially deliver yield and capital growth. The ongoing market reforms from the Equity Market Development Programme should help underpin the market. A revival in Initial Public Offering (IPO) activity should broaden the investable universe, deepen market liquidity, and reinforce investor interest.

Asian bonds: Asian bonds have shown greater resilience even as persistent deficits and rising government debt levels lift volatility in developed market (DM) bonds. Not only are Asian bonds more resilient, but they have also historically delivered competitive long-term total returns. This means that adding Asian bonds to a portfolio of US/global bonds can improve the risk-return balance. Active management is key to navigating the region’s varying credit fundamentals, policy paths, and local market dynamics. Flexible bond strategies that can access both the USD and local currency Asian bond markets, while managing currencies dynamically, are best placed to capture the opportunities within Asian bonds and deliver total returns.

Capital growth

Asia: A broad Asian exposure taps into the region’s structural growth drivers, while a value approach adds resilience through its focus on fundamentals and inherent quality bias. This should be beneficial especially during uncertain or volatile markets. Factor returns over the last 3 and 10 years show that the value and yield factors have performed well in Asia, while the growth factor scores better in the US1. Given its differentiated outcome, a value strategy can provide diversification to US and Asian growth strategies in portfolios.

While a broader Asian strategy can be a core allocation in portfolios, single county strategies may appeal to investors who are looking for undiluted exposure and want to take advantage of a specific macro or earnings cycle.

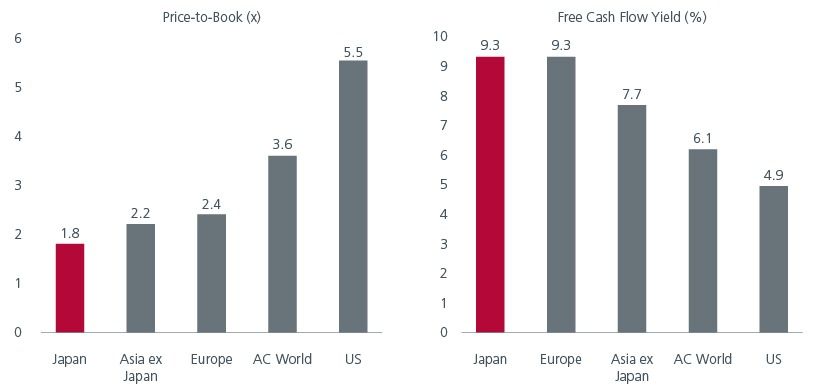

Japan: Prime Minister Takaichi’s landslide victory in February brings about greater policy certainty and a pro-growth agenda. Besides greater government support for the ship building and semiconductor industries, the recovery in global capital spending is expected to underpin earnings in the machinery and automation industries. A potential rise in real wage growth later this year should further support domestic-linked sectors. At the same time, ongoing improvements in corporate governance and capital discipline are likely to continue to lift the market’s return on equity. After the Japanese market’s strong rally in 2025, a value strategy can help investors avoid crowded trades and over-valued stocks while an inherent quality bias can help stabilise portfolios during volatile times. Fig. 2.

Fig. 2. Japan: Valuations are attractive versus other developed markets

Source: Eastspring Investments (Singapore), MSCI Indices, Refinitiv Datastream, as at 31 December 2025. The use of indices as proxies for the past performance of any asset class/sector is limited and should not be construed as being indicative of the future.

India: After underperforming in 2025, the Indian market’s current valuations offer investors a compelling entry point. Macro fundamentals are much improved - Compared to 10 years ago, inflation is at its lowest, foreign exchange reserves have more than doubled, the current account deficit is under control, and fiscal discipline has strengthened. While elevated energy prices, if sustained, could disrupt India’s near-term growth path, favourable demographics, rising incomes, urbanisation, and policy reforms are expected to continue to keep India’s long-term trend growth intact. Notably, India’s frequent policy actions, regulatory decisions and corporate actions create event driven opportunities which can potentially provide greater alpha for long-term investors.

Interesting reads

Sources:

1 Bloomberg factor returns. As of 28 January 2026.

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.