Michael (Xiaochen) Sun

Director, Quant Capability,

Client Portfolio Manager,

Quantitative Strategies,

Eastspring Investments

Apr 2026|5 min read

Executive Summary

- In the current uncertain environment, durable income from equity dividends has become increasingly important; in Asia, dividends have been a reliable contributor to long‑term equity returns.

- Durable income, however, offers little protection if capital is hit by deep drawdowns which is why managing volatility is as essential in a strategy as the dividend discipline itself.

- Staying invested, not timing the market, unlocks the power of compounding, while defensive diversification helps to stabilise portfolios during drawdowns.

Markets have entered a period of heightened volatility as the war in the Middle East raises concerns over energy supply, economic spillovers, and the diverging views on central bank policy. In this environment, the defensive characteristics of low volatility strategies have provided meaningful downside protection; through March 2026, the Asia Pacific ex Japan Minimum Volatility index1 outperformed the broader Asia market by 2.6% while the Global Low Volatility index2 outperformed the broader global market by 2.0%.

Against this backdrop, balancing income, growth and portfolio resilience has become more challenging. Cash yields are increasingly uncertain with the war risking a reigniting of inflation and clouding the rate outlook just as markets had begun to price in easing. Regardless of whether rates fall, hold or rise, the case for durable income from equity dividends has strengthened.

At this juncture, an equity strategy that provides income with less volatility offers a smoother investment journey and helps investors remain invested and benefit from long‑term compounding.

Dividends: A key pillar of long‑term performance

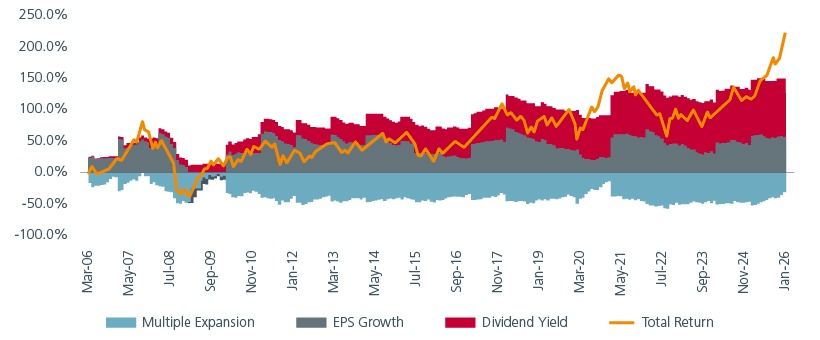

In Asia, dividend yield has been a foundational pillar of long‑term wealth creation. A decomposition of returns for the MSCI Asia Pacific ex‑Japan Index from March 2006 to February 2026 reveals three distinct drivers: earnings growth, valuation changes through multiple expansion or contraction, and dividends. See Fig 1.

While valuation multiples can be highly volatile, swinging sharply between expansion and contraction and acting as both a tailwind and a headwind at different points in the cycle, earnings growth has been comparatively more consistent but remains subject to cyclical variation. Meanwhile the dividend component has delivered the most reliable and steadily compounding contribution to total returns over time.

Fig 1: Decomposition of total returns of the MSCI AC Asia Pacific ex Japan index

Source: Eastspring Investments, MSCI indices, Bloomberg, as of 27 February 2026

A strategy that systematically targets companies with attractive and sustainable dividend yields is therefore not merely seeking income; it is harnessing one of the region’s most reliable sources of total return.

That said, even durable income can be undermined if capital is eroded by severe drawdowns. A portfolio yielding 6% offers little comfort to an investor whose capital base has just fallen by 30%. This is why the second dimension of the strategy, managing volatility, is as critical as the dividend discipline that underpins it.

Volatility: Why managing the downside matters more than chasing the upside

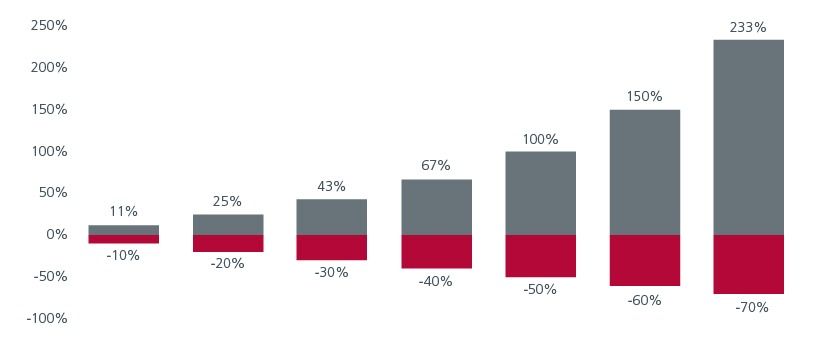

The mathematics of loss recovery are well understood by investors. A stock that falls by 50% must subsequently rise by 100% to break even. See Fig 2. This asymmetry i.e. where losses compound far more painfully than gains, is the single most important reason why managing volatility is critical to long‑term wealth creation.

Fig 2: After a sell off, a greater rise is needed to break even

Source: Eastspring Investments

In practice, however, the real‑world consequences of this return asymmetry are even more dramatic than simple arithmetic suggests. Consider the following striking comparison.

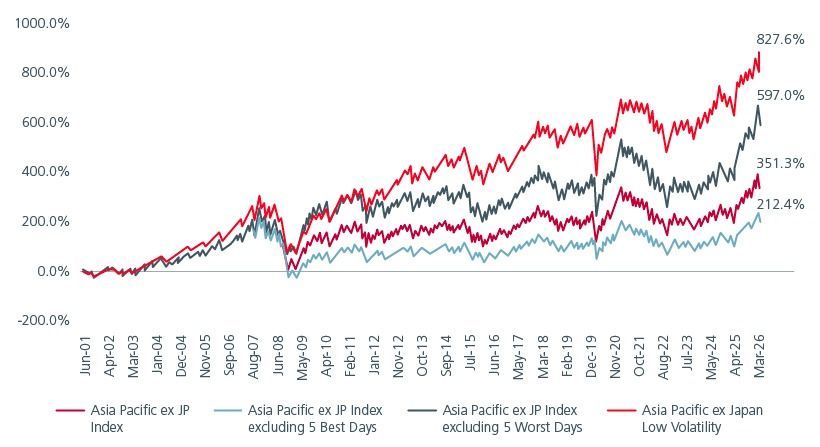

From 1 June 2001 to 20 March 2026, the MSCI AC Asia Pacific ex Japan index delivered a cumulative return of approximately 351%. See Fig 3. Remove just the five worst trading days from the entire period, and the cumulative return rises sharply to around 597%, roughly 70% higher. Conversely, if an investor were to miss the five best days, cumulative returns fall to approximately 212%, some 40% lower.

Fig 3: Asia Pacific ex JP market performance when missing the best/worst 5 days

Source: Eastspring Investments, MSCI indices, Bloomberg, as of 20 March 2026

These figures reveal an uncomfortable truth for investors: a handful of extreme trading sessions, just five days out of more than six thousand, can materially alter long‑term investment outcomes. Crucially, the best and worst days tend to cluster around periods of crisis and recovery, making them all but impossible to time consistently.

The key question is not whether these days can be predicted - they cannot - but whether portfolios can be built to withstand them. This is where low volatility adds value from a portfolio construction perspective.

Over the same period (1 June 2001 to 20 March 2026), the MSCI Asia Pacific ex‑Japan Low Volatility Index delivered a cumulative return of approximately 827%, substantially outperforming the broader market’s 351% and even exceeding a scenario where the market avoided its five worst trading days. This is a powerful reminder that staying fully invested even through periods of sell offs, rather than attempting to time the market, can deliver superior long‑term outcomes. The power of compounding, when supported by a smoother return path, is extraordinary.

Building resilience through defensive diversification

Markets will always be uncertain. Tariff disputes, geopolitical tensions and shifts in central bank policy may dominate the headlines, but volatility will be a constant. In such an environment, the objective is not to attempt to predict the next shock, but to build portfolios that are designed to withstand one.

This elevates the importance of diversification, not simply across asset classes, but within equities through genuinely defensive exposures. When drawdowns are swift and correlations rise is precisely when diversification is most needed; investors benefit from allocations that stabilise overall portfolio outcomes.

Defensive strategies are not about opting out of growth; rather, they are about participating in long‑term equity returns while reducing the behavioural and compounding damage caused by severe drawdowns. Incorporating lower‑volatility, income‑generating equities can help balance portfolios across market regimes, supporting resilience without sacrificing participation in the upside.

Ultimately, defensive diversification serves a simple but powerful purpose, helping investors stay invested. And in an uncertain world, staying invested, through every shock, sell off and recovery, remains the most dependable path to long‑term wealth creation.

Interesting reads

Sources:

1 As represented by MSCI AC Asia Pacific ex Japan Min Vol index and the Asia market refers to MSCI AC Asia Pacific ex Japan Index, as of 20 March 2026.

2 As represented by MSCI AC World

Min Vol index and the global market refers to MSCI AC World Index, as of 20 March 2026.

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.