Executive Summary

- AI capex is expected to remain elevated as hyperscalers are driven by first-mover advantage; falling behind risks losing strategic ground.

- Supply scarcity rather than weak demand is a central theme, with winners defined by their ability to deliver at both speed and scale.

- Efficiency gains in training/inference can lift overall token demand while hardware differentiation could limit oversupply risks.

I recently attended an Asia Technology conference in Taiwan. Technology is an important allocation in our portfolios as the supply chain is uniquely Asian. The semiconductors, advanced packaging, memory, and power infrastructure that underpin the global AI build-out are overwhelmingly produced across the region and in particular in Taiwan, South Korea, and Japan. What is less appreciated is that Asia's technology sector is also a meaningful and growing source of dividend income, offering an even more attractive way to gain exposure to these structural growth trends. Apart from meeting our investee companies, this conference was a great opportunity to connect with our Taiwan-based colleagues to exchange views and ideas.

Is Artificial Intelligence (AI) another bubble?

I started the trip with a central question - Why are hyperscalers still spending so heavily on AI infrastructure, even at peak hardware prices, and when does it stop? While skeptics would call this another bubble in the making, my view is that this cycle is different.

Unlike prior technology cycles, the opportunity for AI disruption is real. Large language model (LLM) monetisation is increasingly visible, token demand is growing exponentially, and there is simply not enough compute to meet it. The imbalance is further compounded by the shift from AI training to inference. Unlike training, inference demand is continuous, scales with user adoption, and cannot be staged the way training runs can.

Underpinning all of this is a first-mover advantage mindset among hyperscalers. Falling behind means losing ground that may be difficult to recover. This is why capital expenditure keeps moving up, even as return-on-investment debates persist.

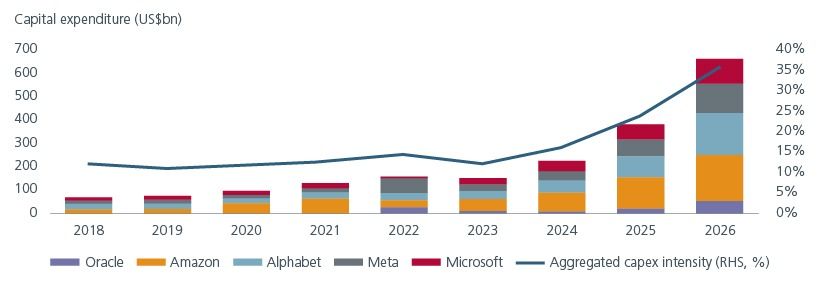

Fig 1: US hyperscalers capex commitments are on the rise

Source: Bloomberg, Apr 2026

Capacity is the new differentiator

As hyperscalers ramp up capital expenditure to secure their position in AI, this surge directly benefits the Asia technology supply chain. The investment narrative has shifted decisively from "is AI demand real?" to "who can actually deliver?" Customers are racing to secure AI compute, and speed to market matters more than price. What stands out in this cycle is the unprecedented pace of technological change. Product roadmaps are evolving continuously, requiring constant engagement at both the company level and in anticipating structural developments.

Capacity expansion was a central theme across discussions. Leading-edge foundry capacity is the primary bottleneck with the tightness percolating throughout the supply chain - from memory and advanced packaging to high-layer printed circuit boards. Availability tightness, rather than demand softness, defines the supply environment. Tier 1 suppliers with the ability to deliver at scale are firmly entrenched, and a growing cohort of companies is proving to be true structural compounders within this ecosystem.

On hardware demand, two developments stood out. The first is the rise of Application-Specific Integrated Circuit (ASIC) chips, a custom-designed silicon which is a credible alternative to Graphics Processing Units (GPUs). The second is the emergence of co-packaged optics (CPO), a new technology that integrates optical components directly into a single package, reducing data centre power consumption. While CPO is unlikely to be mainstream before 2027, it is already shaping hardware content growth and generating new investment ideas.

On memory, the key debate has centred on earnings sustainability, following an unprecedented upcycle since 2024 and a strong run-up in commodity memory prices over the past six to nine months. Memory manufacturers have relied on Long Term Agreements (LTAs) for revenue stability, in which customers soft commit to specified purchase volumes. New LTA agreements are becoming more contractual with negotiations around price and volume commitments, and in some cases, customer prepayments. The extent to which these stronger contractual terms become the norm rather than the exception will determine earnings resiliency as the cycle fades.

Sieving out the noise

Shortly after my trip, a major US technology company published a new data compression algorithm claiming it could reduce LLM memory requirements by six times. Memory stocks sold off sharply as markets feared a collapse in demand. We assessed the algorithm's real-world impact across the AI stack, including its impact on memory requirements to monitoring developer communities for signs of replication feasibility. The algorithm a) optimises only a portion of high-bandwidth memory (HBM) utilisation, b) HBM savings are likely to be meaningfully lower than six times as most LLMs are deployed at reduced precision, and c) has little-to-no impact on storage or system memory requirements.

Our conclusion was that the market overstated the risk. More broadly, our findings reiterated the fact that efficiency improvements of such nature historically tend to stimulate higher token demand rather than reduce it. This episode underscores the importance of evaluating headline developments to distinguish genuine risk from noise, particularly in fast‑moving technology cycles where initial reactions can be incomplete.

Key risk variables

The most debated question is whether hyperscaler capital expenditure intensity falls off. Token demand is growing rapidly, but hardware and software optimisations, such as the compression algorithm discussed above, can flatten the expenditure curve. Such innovations reduce capital intensity but also lower cost to serve and potentially drive token demand. Greater insight into LLM profitability economics, from the upcoming IPOs of major AI developers, will be an important data point to watch.

The second risk is component oversupply as there is sizeable capacity expansion planned in the next few years. When the rising tide fades, who will be at risk? Oversupply issues have prevailed in the past as components were commoditised and fungible. There are signs that hardware components are becoming differentiated and customised to customer requirements. Such differentiation reduces oversupply risk as excess inventory cannot be redeployed elsewhere. This could make the eventual downcycle shallower than those of the past.

Interesting reads

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.