Navin Hingorani

Portfolio Manager,

Global Emerging Market equities,

Eastspring Singapore

June 2024 | 5 min read

Executive Summary

- An Emerging Markets ex China strategy offers greater exposure to smaller, promising markets.

- China’s dominance in the Emerging Markets index crowds out many attractive opportunities.

- A standalone China allocation allows investors to manage their China exposures separately.

1. Given the attractive valuations in China, is this the right time to invest in an Emerging Markets ex China (“EMs ex China”) strategy?

The fundamental reasons for an EMs ex China strategy still hold. China’s dominance in the EM index - where its weight is ~ 27%1 - continues to eclipse the growing opportunities in other EMs and diminishes the correlation benefits of a diversified portfolio. This runs counter to the rationale that investing in an EM portfolio allows one to capture the diverse return opportunities over time.

Concurrently, there are structural factors such as geopolitics, decarbonisation, and shifting economics that are driving supply chains shifts as businesses reduce their reliance on China. Foreign direct investments (FDIs) into China have been slowing while other competing countries have seen their share in global FDIs growing. An EMs ex China strategy is therefore best placed to tap the full potential arising from these supply chain shifts.

Nonetheless we acknowledge that at current valuations, China offers some compelling investment opportunities. To better manage diversification and allocate to less correlated assets investors may be better placed to manage a discrete allocation to China. Recent data points to improving economic conditions in China. However, the road ahead remains bumpy; the ongoing US-China tensions and the pressure from the West about China’s stance on the Russia-Ukraine conflict may continue to impact Chinese corporates. A standalone China allocation allows investors to manage their China exposures and risks separately as well as fully capture upside gains once the market rebounds.

2. Do supply chain shifts from China to other Emerging Markets offer long-term investment opportunities or is it just a short-term thematic play?

A great transition is underway, driven by shifting supply chains, renewed capex cycles across real economy sectors and the decarbonisation revolution. This is a long-term theme, and the transition will yield outsized opportunities for many economies and companies across Emerging Markets. The largest beneficiaries of this transition are likely to be in ASEAN, Latin America, India and EMEA - markets with cheap labour and decent manufacturing bases, and are major producers of key commodities. Most have a large and young population base, and a high economic growth potential which can be exploited by this great transition.

The combined manufacturing value add of these countries is less than half that of China. As such, a small shift of supply chains away from China adds a significant amount of manufacturing value add to these countries.

Moreover, over the last 10 years, companies in both the Developed and Emerging Markets have been under-investing in physical assets (property, plant and equipment) and directing the spending to intangibles, particularly in mergers and acquisitions. Since late 2020 there has been a reversal, and capex spending is on the rise. Historically there is a strong positive relationship between increasing capex spending and the performance of Emerging Markets, with markets outside China benefitting from increased exposure to materials, industrials, and financials.

With green infrastructure being more commodity intensive, there a huge demand for both old and new commodities, many of which can be found in Emerging Markets. As the green capex spend requirements increase, the new spend will be going to hard assets. Emerging Markets are well placed to benefit given that they are global manufacturing bases.

3. Is there sufficient market liquidity in an EMs ex China universe?

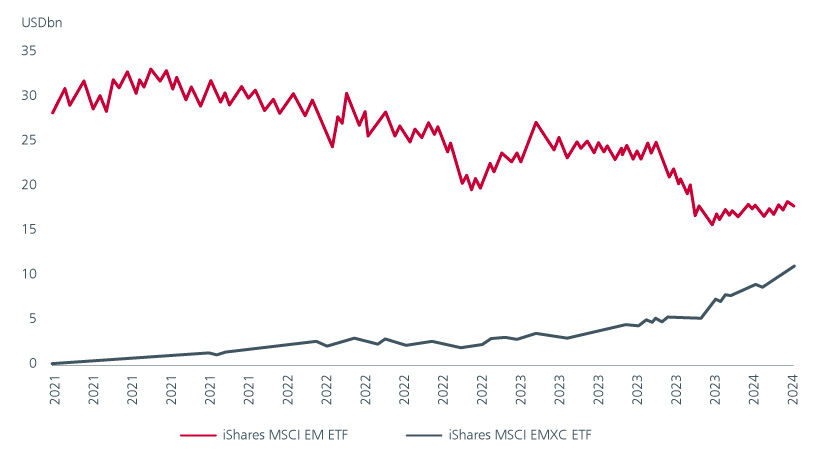

We have seen increasing allocation trends in the last year away from China mandates as investors rethink their positioning here, while we are seeing allocations to EMs ex China equities increase. The assets under management (AUM) of iShares MSCI EMXC ETF is now more than 50% of the AUM of the traditional ishares EM ETF.

Fig 1: Trend of asset flows to EMs and EMs ex China strategies

Source: Bloomberg; Goldman Sachs Global Investment Research, 5 Mar 2024

EMs ex China’s investible universe is sufficiently large with more than 1,200 listed stocks with a market capitalisation of more than USD2bn. This is significantly larger than the EU ex UK and Japan. Emerging Markets excluding China have exhibited comparable liquidity to other major markets with the average six monthly liquidity based on value traded on par with the EU ex UK.

Fig 2: Liquidity conditions in EMs ex China versus major markets

Source: Goldman Sachs Global Investment Research, 31 Mar 2024. ADVT=average daily turnover

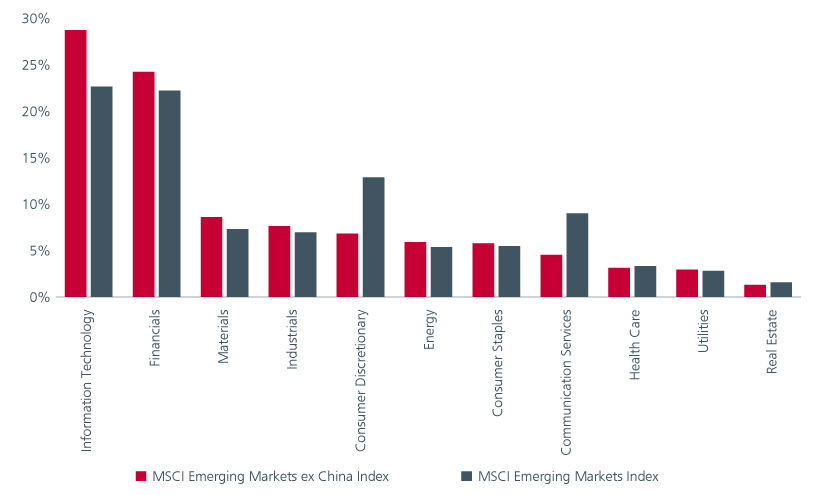

4. With Artificial Intelligence driving recent stock market rallies, can an EMs ex China strategy also capitalise on this theme?

The growth and impact of Artificial Intelligence (AI) is one of the most talked about topics within the corporate world and across investment markets, driving positive sentiment for stocks with earnings related to this theme. AI is very well represented across the EMs ex China universe with substantial representation from the technology sector in the index.

Fig 3: Sector breakdown in the EMs and EMs ex China indices

Source: MSCI indices, 30 April 2024.

Our investment approach is driven by capturing value offered by mispriced stocks that have temporarily fallen out of favour with the market and therefore offer substantial upside potential. Many stocks in the AI universe are richly valued at this time given the popularity of the thematic, however we do find some less well-known stocks and indirect plays with AI-related activities that we believe can outperform over time.

5. Will election outcomes in major Emerging and Developed Markets impact this strategy?

Yes, election cycles can create very interesting investment opportunities for this strategy. Election cycles across Emerging and Developed Markets tend to create volatility in equity markets and EMs ex China are no exception. With elections in the US and India in the headlines during 2024 we would expect that fear of change and uncertainty induces market reactions and over reactions to potential outcomes.

Our approach is to monitor price opportunities in a disciplined fashion looking for those stocks that the market becomes too short-termist and emotional, leading to over selling. Our fundamental analysis focuses on long-term normalised earnings potential of these stocks, and we assess these long-term factors alongside the market’s short-term reaction.

Interesting reads

Sources:

1 MSCI Emerging Markets Index, 30 Apr 2024

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.