Rong Ren Goh

Portfolio Manager, Head of Macro and Thematics,

Asian Fixed Income,

Eastspring Investments

Executive Summary

- With its large number of high dividend yielding companies, a corporate culture that is increasingly focused on shareholder returns and attractive all-in bond yields, Asia is a compelling region for income seeking investors.

- From equity options underwriting to seizing cross currency bond opportunities, there are innovative strategies which active managers can adopt to enhance income.

- Risk management is central especially when taking advantage of income-enhancing tactical opportunities. For end investors, it is important to understand the sources of income – not just focus on a high headline yield.

Many investors look for income from investments, but does it matter where and how that income is generated?

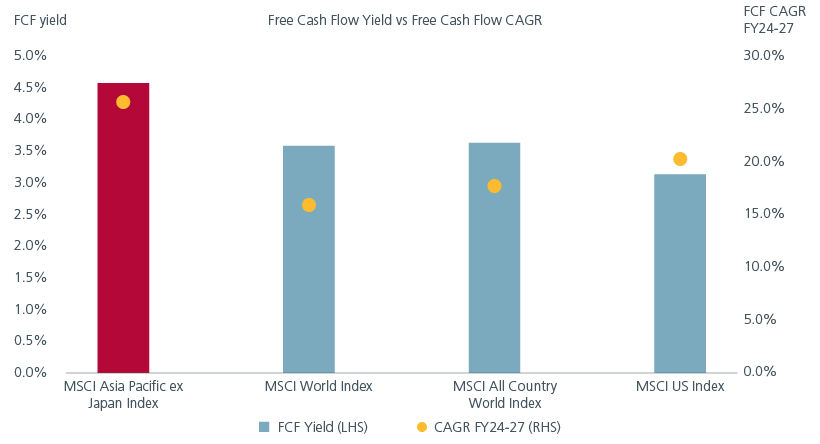

We believe that Asia has unique features that helps it provide investors with quality and sustainable income. Compared to the rest of the world, Asia Pacific ex Japan has the highest number of companies (>400) with dividend yields above 3%, reflecting a strong management culture that focuses on shareholder returns. Asia’s high dividend paying companies are found in both stable as well as high-growth sectors, potentially offering investors income and growth. At the same time, government -led initiatives to improve corporate governance and shareholder returns are rising in Asia. As for Asia’s bond markets, they still offer investors attractive all-in yields. The structural rise in domestic investor participation in some of Asia’s high yielding bond markets such as Indonesia and India have also helped to lower market volatility.

Fig. 1. Asia corporates beat on cash flow metrics

Source: Bloomberg, Eastspring Investments as at 31 December 2024, The use of indices as proxies for the past performance of any asset class/sector is limited. Past performance is not necessarily indicative of the future or likely performance.

Asian economies are also underpinned by a diverse and evolving set of growth engines. Earnings revisions are improving across the region and domestic consumption appears to be recovering in India. Meanwhile Taiwan, South Korea and China are benefiting from their leadership in advanced technology while ASEAN’s prospects are supported by its manufacturing capabilities and tech-adjacent growth.

As active managers tap on Asia’s income edge, there are innovative strategies that can help to boost income, but it is important that they do not compromise on risk.

Q. How are you approaching income enhancement given today’s market environment?

Christina: Our approach is a blend of longer‑term positioning and selective, tactical opportunities. At the core, we maintain longer‑term holdings in income‑generating stocks, where we focus on fundamentals such as business quality, balance‑sheet strength, and cash flow sustainability. Alongside this, we layer on tactical strategies. This can include dividend capture opportunities, where we position around dividend ex‑dates, as well as selectively positioning ahead of sizeable special dividends when we believe the market has not fully priced them in. We also make use of covered calls - writing single‑stock options over existing holdings to generate additional income.

Rong Ren: We are focused on enhancing income through strategies that are repeatable and uncorrelated. One area is option underwriting, where we sell short‑dated, out‑of‑the‑money foreign currency (FX) options to harvest the gap between implied and realised volatility in selected FX pairs. Asian currency regimes tend to exhibit managed volatility and we aim to harvest volatility premia without taking meaningful directional FX risk.

We also seek to take advantage of cross‑currency basis opportunities. When funding dislocations appear, swapping between USD and local currencies can add incremental carry. That said, we only act when the uplift clearly exceeds liquidity and transaction costs.

Q. How do you think about risk management as you look to enhance income?

Christina: Risk management is central, particularly when combining longer‑term positions with more tactical strategies. We are laser‑focused on potential catalysts across our holdings, and that becomes even more important when strategies are shorter‑dated or more tactical. For example, timing is key when using covered calls. Writing options ahead of known events such as earnings announcements can create unintended outcomes, where the option moves in‑the‑money and the costs offsets the premium earned.

By comparison, dividend capture and positioning around special dividends tend to align more closely with our core fundamental skill set. While these strategies are generally less exposed to the risks associated with options, we remain on the look-out for potential catalysts which can cause outsized portfolio downside.

Rong Ren: Agree with Christina that risk management is front and centre when we manage portfolios. In option underwriting, we keep tenors short to limit gap and gamma risk, stay strictly in out‑of‑the‑money strikes, and cap deltas and notionals. This is to ensure that any potential losses are limited. We also avoid executing near major macro events and regularly run stress tests to validate portfolio resilience.

For cross‑currency basis trades, we only take advantage of such trades when the currency moves are driven by technical funding flows. We prefer liquid short‑to‑medium tenors, and size positions accordingly to avoid excessive portfolio volatility. Having clear pre-set exit triggers is important. At the same time, aligning with liquidity needs help ensure basis carry stays incremental rather than directional.

Q. Is there “good” and “bad” income?

Christiana: I believe that there is no “good” or “bad” income, only poorly understood income. If you buy a high dividend stock for the long term but fail to discern that the high dividend yield is a one-off and the stock collapses in the next quarter, then you have misunderstood the stock and have taken on outsized capital risk, despite generating some income in the short term. If, however, you have identified that the same stock is high dividend yielding because of a special situation and you capture this tactically over the short term, and size the position accordingly, then you would have generated income while managing capital risk more effectively.

Rong Ren: For me, good income tends to be transparent, often coming from well‑understood structural premia such as volatility or basis premia. It is typically generated using plain‑vanilla instruments, with clearly defined exposures, and limited tail risks. Good income should also be repeatable and scalable.

By contrast, bad income often looks attractive on the surface but is exposed to deep tail risk, excessive leverage, or have path-dependent, opaque structures. Bad income tends to have liquidity risks, making the trade potentially difficult to exit during periods of market stress, or hinges on a single macro outcome being right.

Q. What are some considerations which end investors should bear in mind when investing for income?

Christina: Be vigilant and discerning. Getting drawn in by a high headline yield can be dangerous if the yield is not sustainable. Invest with managers that have both your capital and income in mind.

Rong Ren: Understand where the extra income is coming from and what the worst‑case outcomes could look like. For institutional investors, any income‑enhancement strategy should sit comfortably within the portfolio’s risk budget and liquidity profile, particularly during periods of stress. These strategies should support overall portfolio resilience, rather than introduce new vulnerabilities.

Interesting reads

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.