Eastspring Investments

May 2026|5 min read

Executive Summary

- AI is becoming a structural growth driver for Asia, anchored by data centre build outs and leadership in tech hardware supply.

- The next phase of AI investing in Asia is less about headline growth and more about the durability of cash flows and returns generated by AI spending.

- AI investing does not favour any one investment style; success hinges on identifying companies that can monetise AI.

Artificial Intelligence (AI) is becoming an increasingly important structural force for Asia. The region’s export strength is now being supported by AI‑related demand, particularly across AI infrastructure, semiconductors, and technology supply chains. Equally, the scale of investment, especially in data centres and supporting infrastructure is significant. Asia is both a key supplier of tech hardware and the second-fastest growing region for data centre capacity.

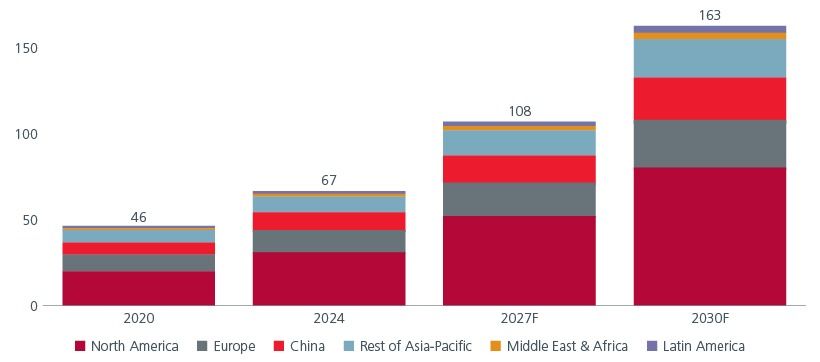

Fig 1: China dominates Asian data centre growth

Source: Bain Data Centre Model, 2025. Notes: Assumes baseline scenario of sector growth; values are rounded

However, the key constraint on AI data centre expansion across Asia is power delivery. The ability to scale efficiently is increasingly shaped by power availability, grid reliability, energy mix, and policy execution. These factors are emerging as key differentiators across Asian markets.

Fig 2: AI data centre potential electricity readiness capacity

Source: IEA Energy & AI 2025; Wood Mackenzie; Deloitte APAC 2026; Ember; IEEFA; Introl/BofA; PwC APAC Clean Energy Gap; SemiAnalysis

Against this backdrop, AI exposure in Asia needs to be selective. Companies supplying the AI investment cycle stand out as the capex boom appears likely to persist despite higher energy prices. Nonetheless the proof lies in earnings delivery as the focus shifts to the durability of cash flows and returns generated by AI spending.

The Q & A with Sundeep Bihani (Portfolio Manager, Regional Asia Value Equities), John Tsai (Head of Growth Equities) and Christina Woon (Head of Equity Income) outlines how they are approaching AI opportunities across Asia.

Q1. Is the AI opportunity in pure plays or adopters?

Sundeep: It is not a simple choice between pure plays and adopters. Focus on durable businesses where AI improves value and lowers costs, avoid value traps, and look to sectors such as industrials, financials, and travel where AI is lifting efficiency without the hype.

John: From a growth perspective, the most compelling AI opportunities are where the pace and scale of growth remain underestimated. In several cases, particularly in Korea and Taiwan, growth assumptions have had to be revised upwards as demand has outpaced expectations.

Christina: For income investors, AI matters only where it supports rising revenues, resilient cash flows, and long‑term income stability. Look for companies funding AI investment from internal cash flows which helps to preserve balance sheet strength and underpin sustainable income generation.

Q2. How can investors spot AI hype versus real earnings impact?

Sundeep: A clear red flag is crowded trades where markets already price in years of supernormal returns. Be wary of theme‑chasing and focus on businesses with a proven ability to navigate past cycles and adopt new technology in a disciplined way.

Christina: AI hype is evident when companies talk about rising AI capex without a clear monetisation plan or visibility on how it will drive revenues, efficiency, and cash flows.

John: Some companies are engaging in AI‑driven capex races out of fear of falling behind competitors, reinforcing the need to look past the narrative and focus on the numbers.

Q3. Which business models are most at risk of value erosion due to AI?

Sundeep: Businesses that rely on large, fixed investments but face rapid AI‑driven substitution are particularly vulnerable. This is why an active approach is needed to pick the winners.

John: AI has the potential to accelerate competitive shifts, with rapid breakthroughs resetting winners far faster than in previous technology cycles and eroding established advantages sooner than investors expect.

Q4. Have you incorporated AI tools in your investment process?

Christina: AI is primarily used to improve research productivity by speeding up the information processing and surfacing key risks earlier. AI acts as a tool to improve efficiency, not to replace judgement and decision-making.

Sundeep: The team uses AI primarily as a risk management tool rather than for stock selection, stress‑testing whether a business can be made obsolete in the next three to five years. These insights are then reflected in valuation work and assumptions around normalised earnings.

John: With traditional sell‑side research becoming less differentiated, AI can improve internal analysis efficiency and enable greater experimentation.

Q5. What are the key implications for investors?

For growth investors, the challenge lies in distinguishing companies already monetising AI from those investing with uncertain payback. Rising AI budgets and rapid infrastructure deployment support a selective approach, although faster earnings growth, particularly in the US, has made valuations harder to anchor.

From a value perspective, AI can reshape the earnings trajectory for low‑growth or cyclical businesses by improving efficiency, costs, and customer value. With AI expectations in Asia still relatively conservative, valuation discipline, margin of safety and normalised returns remain central.

One of the biggest misconceptions for income investors is that AI is less relevant as a theme because it is capex heavy. However, many companies in Asia, especially those that play into the AI capex boom, are beneficiaries of AI via rising revenues and cash flows, and consequently dividends. The key is to identify the right ones through active stock picking.

Interesting reads

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.