Executive Summary

- Asia’s positive macro environment, strong earnings momentum and rising focus on shareholder return provide a strong and durable foundation for dividends.

- Unlike other regions, Asia’s Technology sector is a key dividend contributor, allowing high‑dividend strategies to capture both attractive income and growth opportunities.

- Asia’s dividend stocks have lower correlations with developed‑market dividend equities as well as Asian and global bonds, offering meaningful diversification for income portfolios.

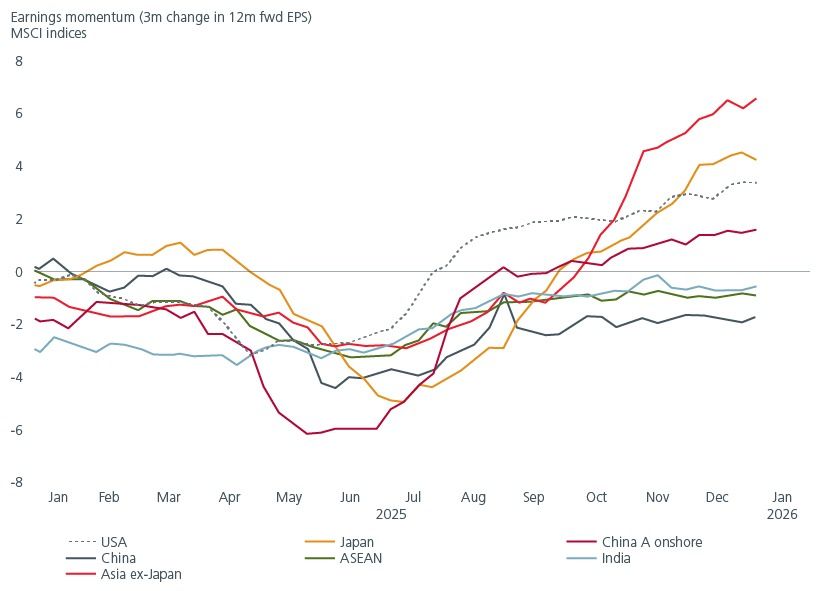

Fig. 1. Asia’s earnings momentum is accelerating

Source: LSEG Datastream. January 2026.

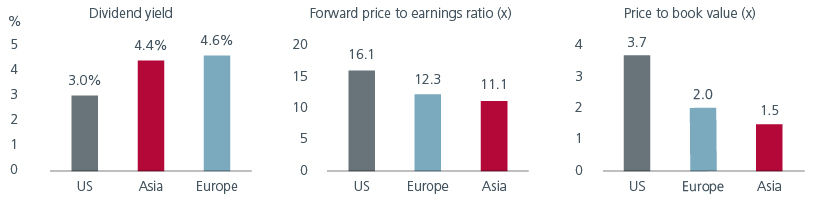

Fig. 2. Asia has attractive dividend yield and cheaper valuations

Source: MSCI. As of December 2025. Asia: MSCI Asia Pacific High Dividend Index. US: MSCI USA High Dividend Index. Europe: MSCI Europe High Dividend Index. Developed Markets: MSCI World High Dividend Index. Past performance is not indicative of future returns.

Asia’s positive macro backdrop is reinforced by a growing emphasis on shareholder value creation across the region. In 2024, South Korean regulators put in place a Value-Up Programme designed to address the undervaluation of Korean stocks and incentivise better shareholder return policies. Since then, similar programmes have been rolled out in India, China and most recently in Singapore. The actions by Asian companies to drive better shareholder returns have been rewarded by the markets. The greater focus on shareholder returns has also led to lower dividend volatility.

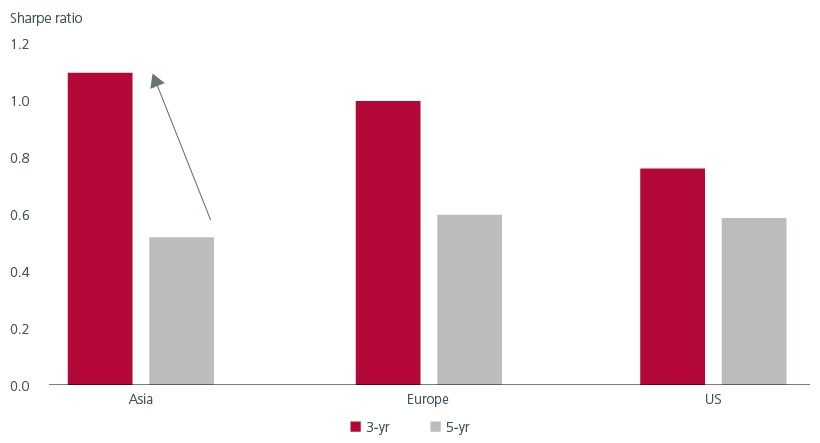

All this, coupled with lower starting valuations, has helped to lift the risk adjusted returns from Asian dividend stocks. The 3-year risk adjusted returns from Asian dividend stocks have improved significantly and are higher than the developed markets. Fig. 3.

Fig. 3. Asian dividend equities offer superior risk adjusted returns

Source: MSCI. As of December 2025. Asia: MSCI Asia Pacific High Dividend Index. US: MSCI USA High Dividend Index. Europe: MSCI Europe High Dividend Index. Developed Markets: MSCI World High Dividend Index. Past performance is not indicative of future returns.

Differentiating Asian income

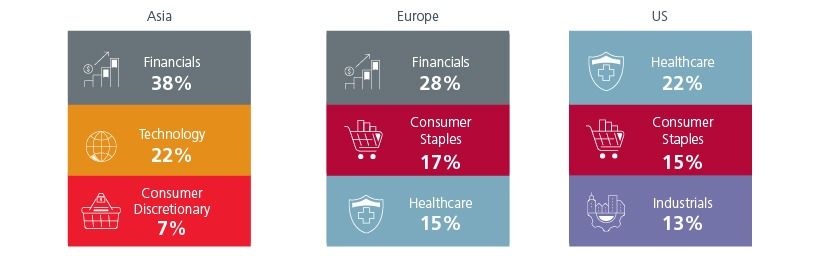

One unique factor that sets Asian dividends apart is that the Technology sector makes up a substantial share of the high dividend yield index in Asia, unlike in US and Europe, where the Consumer Staples and Healthcare sectors are more prominent. Fig. 4. As such, investors in a high dividend yielding strategy in Asia can potentially also gain some exposure to Asian tech companies and enjoy both dividends and growth.

Fig. 4. Breakdown of high dividend indices (largest 3 sectors)

Source: MSCI. As of December 2025. Asia: MSCI Asia Pacific High Dividend Index. US: MSCI USA High Dividend Index. Europe: MSCI Europe High Dividend Index. Developed Markets: MSCI World High Dividend Index. Past performance is not indicative of future returns.

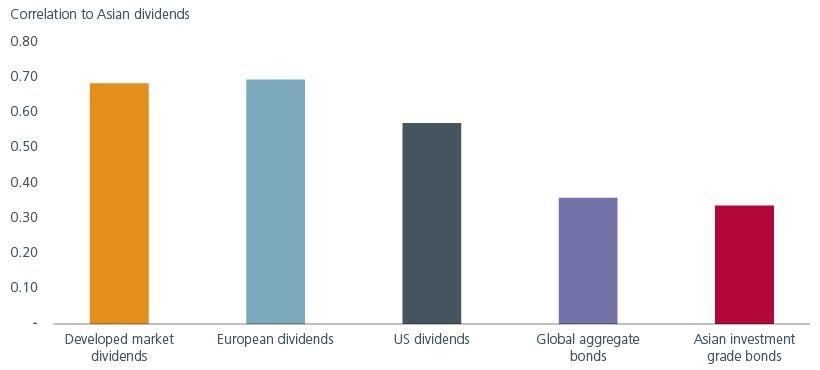

It is also notable that high dividend yielding stocks in Asia have lower correlations to high dividend yielding stocks globally, as well as to global and Asian bonds. This suggests that adding Asian dividends to a global income portfolio can provide investors with greater portfolio diversification. Fig. 5.

Fig. 5. Asian dividends’ correlation with other income producing asset classes

Source: Bloomberg. 10-yr correlation as of 2 February 2026. Asia dividends: MSCI Asia Pacific High Dividend Index. US dividends: MSCI USA High Dividend Index. Europe dividends: MSCI Europe High Dividend Index. Developed Market dividends: MSCI World High Dividend Index. Global aggregate bonds: Bloomberg Global Aggregate Total Return Index. Asian investment grade bonds: JACI Investment Grade Total Return Index. Past performance is not indicative of future returns.

The diversity of dividend payout ratios and yields across Asian countries and sectors creates a rich opportunity set, but we believe that an active approach is needed to fully capture its potential while managing downside risks. Deep fundamental research can help to identify emerging income opportunities linked to structural trends or cyclical sector recoveries. It can also help to seek out opportunities potentially missed by passive or screen‑based strategies. This includes companies that do not currently feature on traditional dividend screens but are approaching an inflection point where they may resume dividend payments, as well as companies which have the necessary conditions and capacity to deliver special dividends.

Equally important, we believe that rigorous bottom‑up analysis can proactively help to identify risks to dividend sustainability, which may arise from deteriorating fundamentals, industry disruption or regulatory change. This would facilitate a reallocation of capital from names where dividend risk is rising into higher‑quality opportunities. Active managers can also deliver incremental income through innovative strategies such as making use of covered calls - writing single‑stock options over existing holdings to generate additional income.

Closing the underweight to Asian income

For income focused portfolios, an underweight to Asia risks overlooking some of the most attractive dividend equity opportunities available today. The breadth of income sources across the different sectors and countries in Asia provides both diversification and resilience in a shifting macro landscape. This is especially important when geopolitical tensions, tariff headlines and shifts in central bank policies are starting to shape the markets in 2026. For investors looking to diversify and take advantage Asia’s attractive equity valuations, dividend buffers come in handy in supporting total returns during periods of market volatility.

Interesting reads

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.