Executive Summary

- Downward pressure on the US dollar is mounting as the US economy is expected to slow more than Asia’s and interest rate differentials turn more unfavourable.

- The weakening US dollar, combined with the high valuations of US assets make the case for investors to diversify into more attractively priced Asian markets.

- Besides diversifying portfolios and using equity options to participate in the market upside, our three-pronged risk management framework ensures that we manage risks proactively.

In a recent event for Singapore-based institutional investors, we shared out thoughts on the economy and discussed new asset allocation considerations amid the changing market landscape. Here are some of the key takeaways.

Q. Why have equity markets trended higher since the start of the year despite tariff uncertainty and geopolitical tensions?

Equity markets have performed better than expected this year for three main reasons.

First, monetary policy support for markets has been highly favourable - 19 of the world’s 22 largest central banks have eased monetary policy over the past 10 months, including 100bps of cuts by the US Federal Reserve (Fed) late last year. Meanwhile, with the Fed expected to cut rates, this can continue to support asset prices.

Second, delays and temporary exemptions to the US new tariffs limited their increase in cost to the US economy to only 0.2% of GDP in January – July.

Third, this delayed tariff impact allowed earnings in the second quarter to surprise to the upside, driving positive revisions to earnings expectations.

Looking forward, tariffs are likely to be an increasing challenge to growth. In the US, the increase in tariff collections is rising with July collections annualizing to 0.8% of GDP. The recent trade deals increase the US’ statutory tariff rate from about 14% to close to 18% effective August 7 -11. And Section 232 investigations concluding in the fourth quarter will push this statutory rate even higher from early 2026. The economic drag from the tariffs on the US will become more pronounced and the ultimate impact on company margins and US inflation could be a potential source of market volatility.

Q. Why is it increasingly important for investors to diversify beyond US assets?

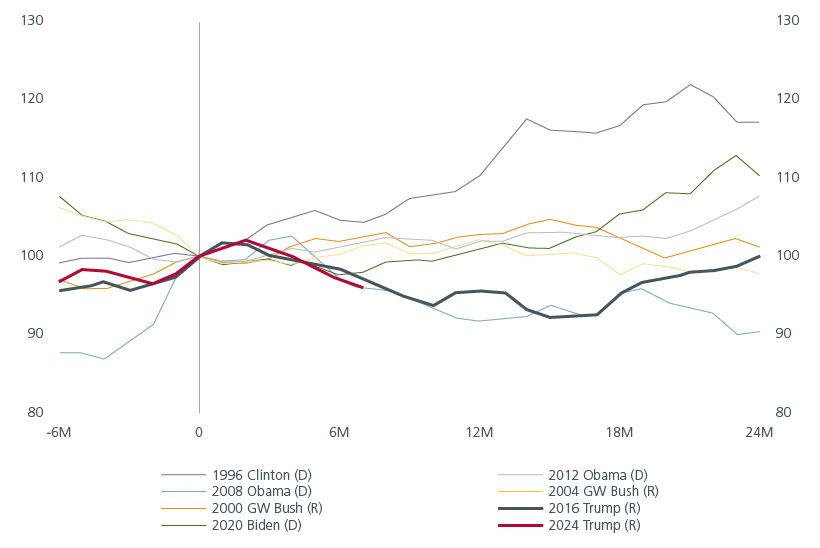

Historically, the US dollar (USD) has served as a diversifier during equity downturns, but this role is being questioned. The USD is expected to trend lower over time, although consensus views should be approached cautiously. The dollar’s trajectory is influenced by relative GDP growth: when US growth lags Asian growth, the dollar tends to weaken. This scenario is unfolding, with the US economy expected to slow more than EM Asia. Interest rate differentials are also moving against the USD, and political factors including a more dovish Fed chair in 2026 add to the downward pressure. It is interesting to note that the USD is following the path it took in the first year of President Trump’s first term, which was also a year of policy turmoil and slower US economic growth. See Fig. 1.

Fig. 1. US broad effective exchange rate

Source: LSEG Datastream. August 2025. Index, election date = 100. 6M before 20 24 after the presidential election.

At the same time, US equities and credit are currently among the most expensive markets globally. While this does not guarantee a downturn, it raises the risk of a “risk-off” episode in which valuations correct. Diversification is essential to manage this risk.

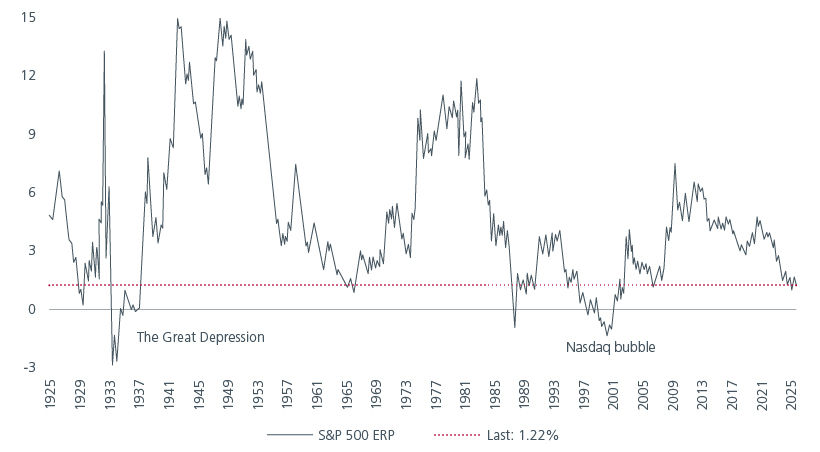

Notably, the US equity risk premium is extremely low, and although it has dipped lower in the past, current levels suggest limited upside for US equities. See Fig. 2. Other markets, including Japan, China, and some of the smaller Asian markets, are showing positive earnings revisions and are not as richly valued. Moreover, dollar weakness has historically supported non-US assets. As the US economy slows more than emerging Asia, interest rate differentials may move against the dollar, enhancing the appeal of Asian assets. Diversifying away from the US allows investors to tap into regions with better valuations and growth prospects such as Asia and the Emerging Markets (EM), while also managing portfolio risks more effectively.

Fig. 2. S&P 500 Equity risk premium since 1925

Source: The use of indices as proxies for the past performance of any asset class/sector is limited and should not be construed as being indicative of the future or likely performance of the Fund.

Q. Should Asia-based investors consider hedging their USD exposures?

Fed rate cuts and slower US economic growth point to stronger Asian currencies which makes hedging USD exposures increasingly relevant for Asia-based investors. In addition, the USD currency that is traditionally considered a diversifying asset that performs during risk-off events, is behaving differently in the current risk regime which makes it unattractive to hold as a diversifier. As a result, investors must weigh the costs of hedging and the potential upside when thinking about their exposures to USD-denominated assets. For USD bond allocations, using bond futures instead of cash bonds can help reduce the need for currency hedging while still benefiting from falling yields.

For Singapore dollar (SGD)-based investors, although the SGD is currently at the top of its trading band, it can potentially strengthen further against the USD if the dollar weakens against the euro and yen. SGD-denominated bonds have outperformed peers in the developed markets in the first half of 2025 and continue to attract investors who are seeking quality and stability. At the same time, the Singapore equity market is a relatively defensive lower beta market which offers attractive valuations and high dividend income from Real Estate Investment Trusts and the banks. While US Investment Grade credit and Treasuries used to be an attractive proposition for their higher yield as well as currency diversification, this investment thesis has weakened more recently given the tight credit spreads and weaker USD expectations.

Q. What are the potential risks facing global markets?

Some key risks include the uncertain implementation of tariff rules or that Trump surprises with more aggressive than expected sectoral tariffs in Q4 2025 and Q1 2026 as the result of current Section 232 investigations. For Asia specifically, a risk is that Asian trade deals with the US create tension with China because of requirements to impose tariffs or other impediments to trade with China.

At the same time, geopolitical tensions still loom. Supply-side inflation shocks may emerge in the near-term, which could raise inflation expectations. That said, we note that these events have historically not had a long-lasting impact on risk assets.

Meanwhile, China’s growth slowdown continues to weigh on global growth. China’s economic recovery requires more substantial and targeted stimulus. The property downturn continues to stress households, while persistent deflation risks global spillovers. We expect the Chinese government to support growth through increased subsidies and other measures. However, a shift towards fiscal consolidation could lead to an earlier-than-expected slowdown.

There are also upside risks which include, but are not limited to, the US economy proving to be more resilient to tariffs than expected. The Fed could also cut more than expected, causing risk assets to melt up.

Q. How are you managing portfolio risks in the current environment?

We are diversifying portfolios across asset classes and geographies. Where possible, we are using equity options to participate in the market upside while limiting the downside. We are also diversifying into gold and Treasury inflation-protected securities (TIPs) to hedge against stagflationary risks.

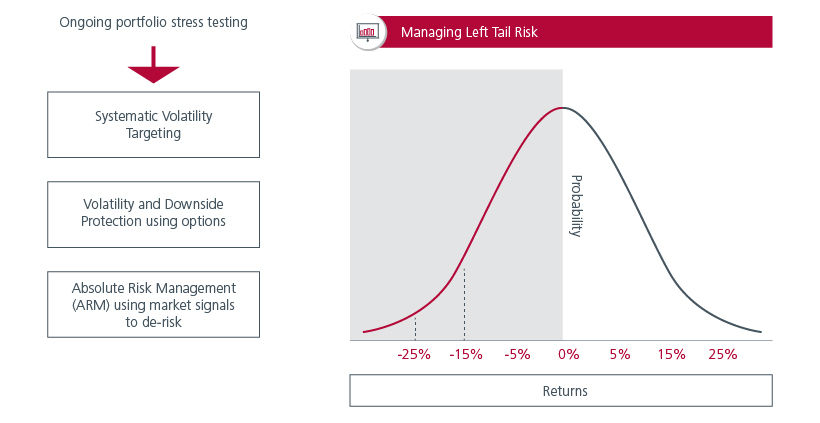

We manage risk proactively, not reactively. For portfolios with a total return mandate, we stress test the portfolios regularly to assess resilience across different economic and market scenarios. Our three-pronged risk management framework (See Fig. 3) includes Systematic Volatility Targeting, where we derisk the portfolio if any asset classes display unusually high levels of short-term volatility, independent of the underlying cause. We also seek to protect portfolios opportunistically via option strategies, guided by market pricing or stress test outcomes. For example, we would purchase cost-effective protection for portfolios rather than reacting to market events. Meanwhile, we practice Absolute Risk Management where we leverage back tested market signals to derisk and raise cash when warranted.

Fig. 3. Protecting portfolio’s absolute return

Source: Eastspring Investments. For illustration only.

Interesting reads

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.